Modelling the local economic impacts of the coronavirus

The COVID-19 pandemic is a health crisis, which is quickly turning into a major economic shock. It affects all sectors of the economy, to varying degrees.

Here Ben Gardiner and Chris Thoung looks at three aspects of the economic impact of COVID-19 from a local point of view: economic exposure, impact, recovery and resilience.

Economic exposure

At a local level, lock-down and social distancing are causing immediate challenges of unknown duration, but the degree of economic exposure a local area faces will largely depend upon two factors:

- The sector-occupation-mix: the structure of a local economy, and the effects of the lockdown on dependent industries (possibly elsewhere in the world) as well as the impact of a country’s own measures.

- At the worker and firm level: the likelihood of remaining employed or in business, as well as the ability to financially withstand a lockdown. With income or salary support still to be paid can people and businesses hang on long enough?

So, local exposure depends on the relative concentration of vulnerable workers, firms and industries.

To help assess the scale and duration of the COVID-19 impact, the Office of Budgetary Responsibility (OBR) has produced an illustrative UK macro-sectoral scenario which assumes a 35% fall in GDP in 2020(Q2) followed by a bounce-back, leading to a fall of 13% for the whole year.

Cambridge Econometrics has developed its own set of more detailed and consistent macro-sector projections (forthcoming) under alternative recovery paths, using our global macro-sector model (E3ME). These projections do not show an immediate bounce-back and return to normality.

But to reiterate, using a sectoral structure to predict local effects is only part of the story, modelling needs to be localised to consider a range of possible outcomes and our team has already started looking at the local vulnerabilities to the economic impact of COVID-19 across Great Britain.

Wider economic impacts

Using our Local Economy Forecasting Model (LEFM), Cambridge Econometrics can produce estimates of the direct sector employment and GVA impacts by combining local intelligence with analysis of:

- an area’s specific business demography (e.g. which sectors are most likely to be affected and by how much, which depends on the business make-up (size/sectors) in the local area)

- the occupations of the workforce

- the impact the spread of COVID-19 is having on participation on the local workforce

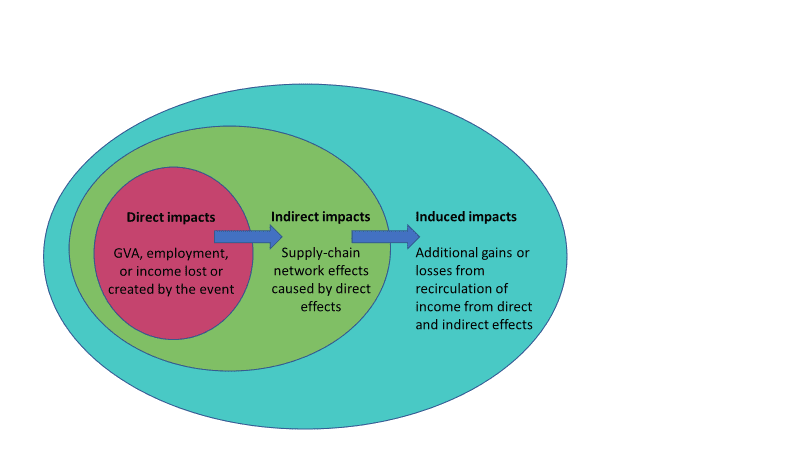

The analysis can also consider offsetting factors, such as where jobs have been gained in other sectors, such as health and care sectors. These are combined together in the model’s input-output framework which measures the extent to which supply-chain effects are important for different industries and locations.

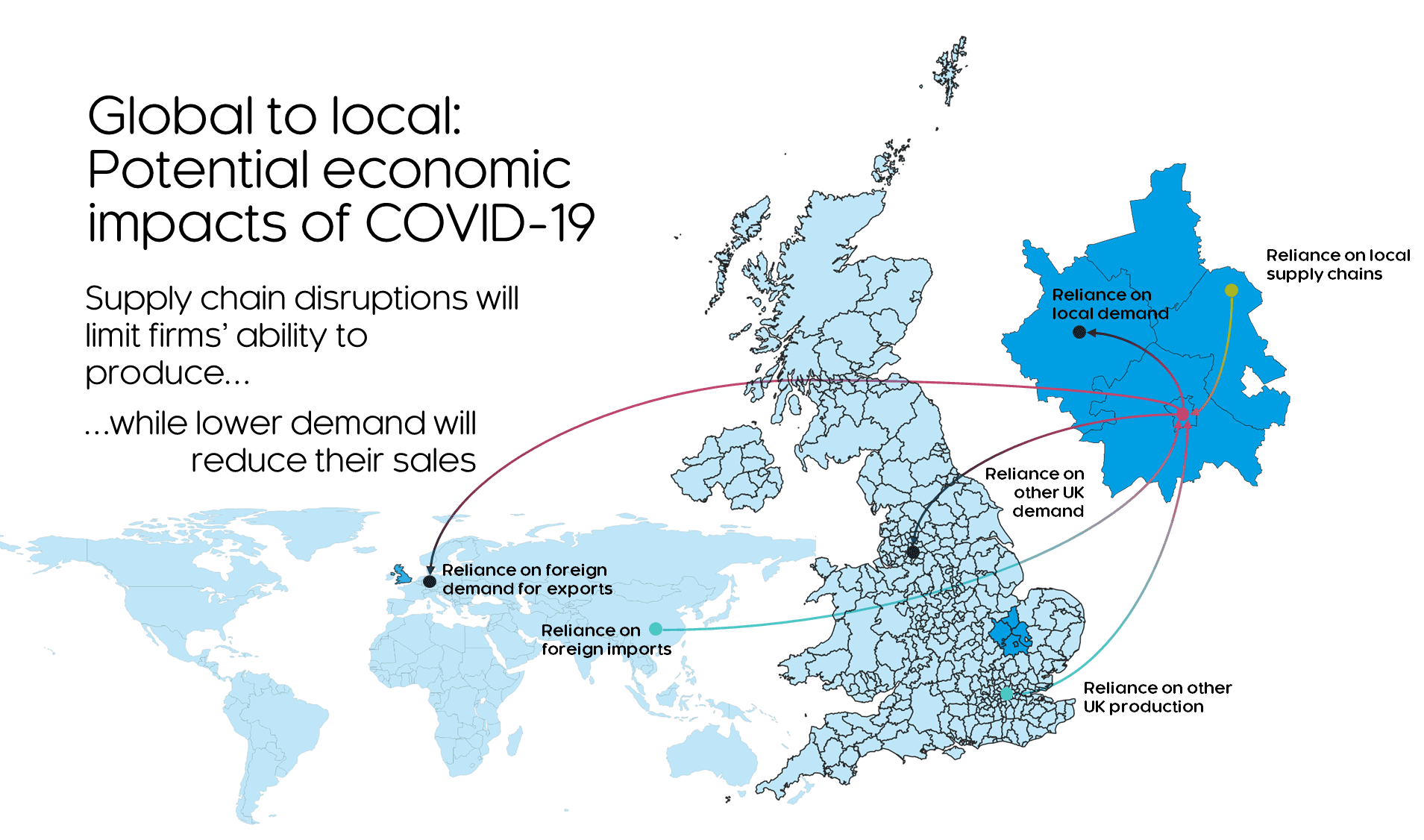

The overall impacts include the direct, indirect (supply-chain) and induced (additional spending) effects – as shown in the figure below:

For example, if we consider an area’s hospitality sector (covering hotels and restaurants), which is one of the most-highly affected sectors due to the travel and tourism restrictions currently in place, there will initially be an estimate of how many jobs have been affected from surveys, business network information, or more official government sources such as the HR1 redundancy notifications.

From there, the LEFM model can estimate the knock-on effects to suppliers in other sectors, in this case principally manufacturers of food and drink and business services (used for marketing purposes).

Finally, the people directly employed in the hospitality sectors and their supply chains will spend some of their incomes on other goods and services, often in the local economy (for example, in retail and leisure outlets). All these components can be combined together to gauge the total estimated local impact.

Cambridge Econometrics can work with you to ensure the assumptions about the supply chains for local sectors (what goods and services are used and importantly, the extent to which they are sourced locally) best represent the reality. We can provide local economic impacts in terms of:

- Employment, output (GVA) and productivity by detailed sector

- Employment by occupation

- Household income and consumption

Recovery and resilience

While vulnerability to the economic shock of COVID-19 and its wider impact are important aspects to consider, equally important is how well-equipped different sectors and geographies are to adapt and recover from the shock, and this relates to the concept of resilience.

Work by the Citi-Redi team at the University of Birmingham has done some preliminary analysis, looking at factors which influence local area resilience and linking them to both previously identified factors associated with resilience and also performance from the last big shock, some ten years ago now.

Other research undertaken with the University of Cambridge puts forward three conclusions which are also relevant for the Covid-19 crisis and emerging shock:

- There is rarely a bounce-back where above-trend or faster growth is enjoyed. In other words, the hit to output and/or employment is permanent and not recovered

- The effects of shocks (both ability to resist and recover) are compounded by other (slow-burn) effects already going on in an economy – so areas which are suffering from industrial decline, those seen as ‘left-behind’, or which might be experiencing the early adverse impacts of Brexit, are likely to suffer greater disruption from the added effects of COVID-19

- How well an area was able to resist previous shocks can have little bearing on how well they recover from the next one that comes along – this finding is related to the different nature of shocks and the varying impacts that result

One thing that is understood about resilience is that each shock is different so different factors might be important in determining how well economies adapt and recover, and this is particularly important for lower level geographies where differences become greater as spatial scale decreases.

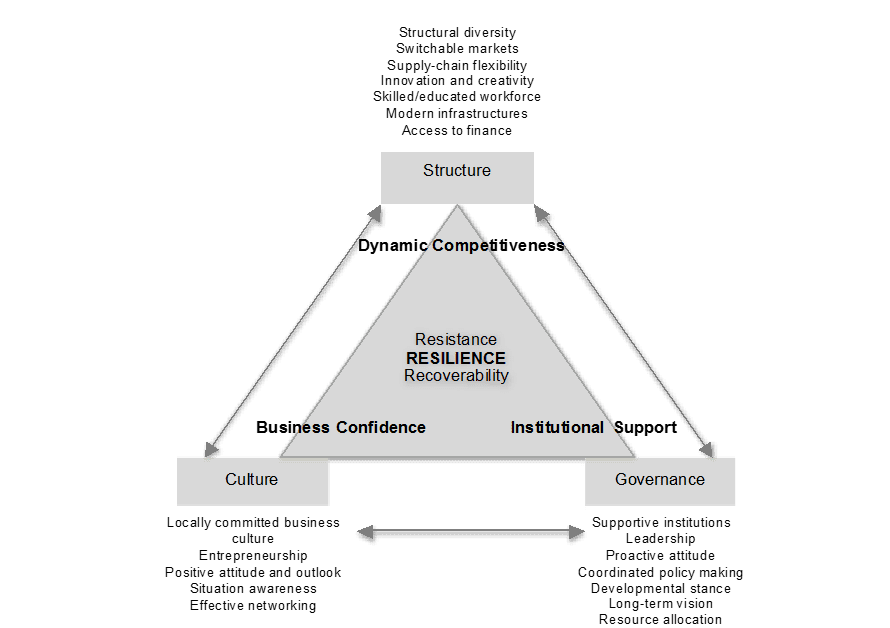

Work undertaken by Cambridge Econometrics for the Core Cities Group considered resilience to shocks, and used the approach summarised below to show how building economic resilience for sustained recovery will entail focusing policy simultaneously on at least three main aspects of a city’s economy.

The various elements and fundamentals (the industrial ‘ecosystem’) that promote local dynamic competitiveness; a local economic environment and culture that inspires business confidence and commitment; and a local institutional system of support and leadership, with a collective vision for the city’s development.

None of these policy dimensions can be resolved overnight, and will take substantial resource and time to change, as well as a continuation of the devolution agenda to give local policy makers the power to make changes at appropriate levels of governance.