Carbon-neutral steel production: is it a possibility?

Quite literally, steel is the backbone of a modern society. Unfortunately, the production of steel contributes significantly to human-made climate change. It is very unlikely society will cease to demand steel, so it is important to figure out how the iron and steel industry can be incentivised to employ low-carbon technologies.

Cambridge Econometrics has incorporated a series of models of technology diffusion, FTT, which are applied to a range of different energy sectors. The FTT models are based on innovation theory and evolutionary dynamics. FTT:Steel is the latest addition to the series and with it we can assess questions such as: Can we sensibly decarbonise the iron and steel industry?

What technologies would emerge as a result of policies aimed at climate change mitigation? And not entirely unimportant, what are the impacts to the economy when these sorts of policies are implemented? FTT:Steel can also be used to investigate questions related to resource efficiency, raw material extraction, and circular economy among others.

The steel industry is highly carbon-intensive

Being responsible for five to eight percent of all emissions, one-third of all industrial emissions, and the consumption of roughly thirty percent of all unearthed coal, the need to change the steel industry is evident. The pathway to facilitate this change, however, is not. Present-day steelmaking predominantly revolves around using fossil fuels to convert iron ore to metallic iron. Greenhouse gas (GHG) emissions are inevitable in these processes. The second-most dominant steelmaking technology consumes electricity almost exclusively and uses steel scrap as feed material. The added benefit here is that there is no need for downstream processes, such as unearthing the iron ore and subsequently reducing it to metallic iron.

Yet, this is not the answer to decarbonise the steel industry. In theory steel is fully recyclable, but in practice it can be difficult due to contamination with other metal scrap (e.g. copper) and the use of coatings on steel products (e.g. zinc-based coatings). More importantly, steel demand is projected to outweigh scrap supply up to 2050 (based on Pauliuk, et al. (2013) and own calculations). This means alternative steelmaking routes are needed.

What are the alternatives?

Various novel steelmaking routes have been proposed. Some of them focus on including lower quality materials (e.g. direct reduction technologies, or smelt reduction technologies such as COREX), others on reducing emissions that contribute to particulate matter formation (e.g. FINEX in South Korea). A few new production pathways have recently emerged that reduce direct GHG emissions:

- Advanced smelt reduction (HIsarna pilot plant in the Netherlands)

- Biobased steelmaking (e.g. Brazil)

- Carbon Capture and Storage/Utilisation (CCS/U) (pilot plant in United Arab Emirates)

The abovementioned technologies reduce emissions to some degree but have their limitations. Advanced smelt reduction manages to reduce emissions by 20% compared to conventional steel production. Biobased steelmaking is essentially emission-free when the take up of GHG by trees is considered, but in conventional processes it cannot replace fossil resources fully and then there is land-use change and land competition with agriculture that should be considered. Lastly, CCS/U is often mentioned, but geological storage capacity is limited and scrutinised by the public.

Then there are two further processes in research phase at the moment:

Both are free of direct GHG emissions, but emissions may occur elsewhere during the production of hydrogen or the generation of electricity. The former is gaining traction in the real world. After a successful pilot stage of a hydrogen-based direct reduction (DR-EAF (H2)) plant in Sweden, the HYBRIT consortium has announced to invest heavily in a the first large scale green hydrogen-based steelmaking value chain, which includes electrolysers, hydrogen storage facilities, and wind parks. Other hydrogen steel projects have been announced or are in progress in other parts of the world as well( e.g. in Germany (Thyssenkrupp) and in Austria (Voestalpine)).

How do policies affect technology uptake?

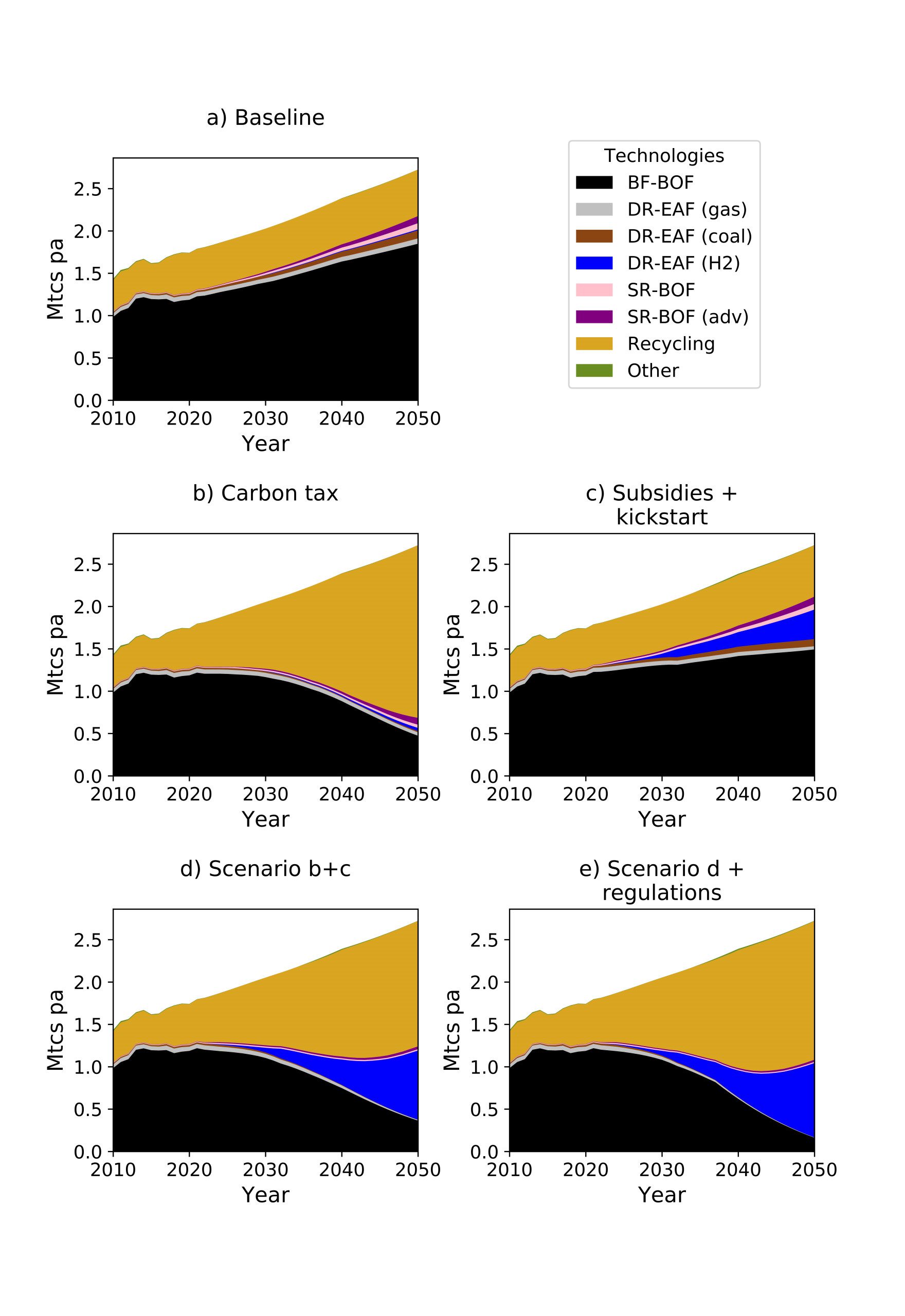

Various policy pathways can be pursued to bring about decarbonisation (excluding demand-side policies) these are designed to either incentivise low-carbon technologies or to penalise carbon intensive technologies. Examples of the former are subsidies on capital investment costs or the use of specific energy carriers. In the latter case, carbon taxes or regulations and even the phasing-out of specific technologies could be options. The figure below shows the effects of several policies on the diffusion of technologies. When no policies are implemented (panel a of figure 1), the most commonly used steel production routes at present remain dominant (the blast furnace – basic oxygen furnace combination, BF-BOF), while only small-scale market penetration can be observed for a relatively new, less carbon intensive production method in three decades from now.

Applying a carbon tax to just the steel sector seems an unlikely policy lever, so when we speak of a carbon tax it applies economy-wide and therefore includes and affects other industries. A carbon tax will obviously affect the most carbon intensive routes (panel b). Investors will be looking for new technologies that can avoid the extra burden a carbon tax poses. One such route already exists, and it involves the recycling of steel.

However, its rise to market domination will push other novel technologies out of the way. Why is that a problem? Steel recycling is inherently a low carbon, less energy intensive steel production pathway, but as stated before, the scrap supply is limited, therefore low-carbon, secondary steel production is limited and low-carbon, primary steel production a necessity.

Something else is needed to promote low-carbon, primary steel production

Instead of penalising carbon intensive technologies, the focus should shift to promoting novel, low carbon technologies.

Subsidies on capital investment and on hydrogen and electricity consumption, in conjunction with a kick-start policy of such technologies could help. Panel c does show greater uptake of novel technologies compared to the carbon tax, but emissions do not decrease. This can be attributed to less of the investments flowing into secondary steel production, and in this scenario, investors are not incentivised to move away carbon-intensive, primary steel production.

Subsidies alone are unlikely to change the status quo of the locked-in position of the two most dominant technologies. How would technology uptake under a combination of the two preceding policies look like? Panel d shows that we again see a dominant position of secondary steelmaking, with more additions of novel, low carbon primary steelmaking at the cost of present day’s dominant primary steelmaking route. Greater emission reductions can be achieved with the combination of technology-push and market-pull policies, than either alone.

In all of the preceding scenarios we observed that the conventional blast furnace – basic oxygen furnace route still holds a prominent position in the global steel market. What would happen if we applied phase-out regulations on this production route in conjunction with the previous set of policies? Panel e of figure 1 shows that the carbon intensive technologies are phased out at a slightly faster rate compared to scenario d, which paves the way for greater uptake of low-carbon technologies.

Figure 1: Development of various technologies over time under the influence of different policies. BF – BOF: Blast furnace ironmaking in combination with basic oxygen; DR – EAF (gas): Gas-based direct reduction ironmaking in combination with electric arc furnace; DR – EAF (coal): Gas-based direct reduction ironmaking in combination with electric arc furnace; DR-EAF (H2): Hydrogen-based direct reduction in combination with electric arc furnace; SR – BOF: Smelt reduction ironmaking in combination with basic oxygen furnace; SR – BOF (adv): Advanced smelt reduction ironmaking in combination with basic oxygen furnace; Recycling: Production of steel in an electric arc furnace, with steel scrap as input. Different variants for each of these technologies exist which may incorporate carbon capture and storage or utilisation or replace (some of its) fossil resource input with biomass.

How does this affect emissions and the economy?

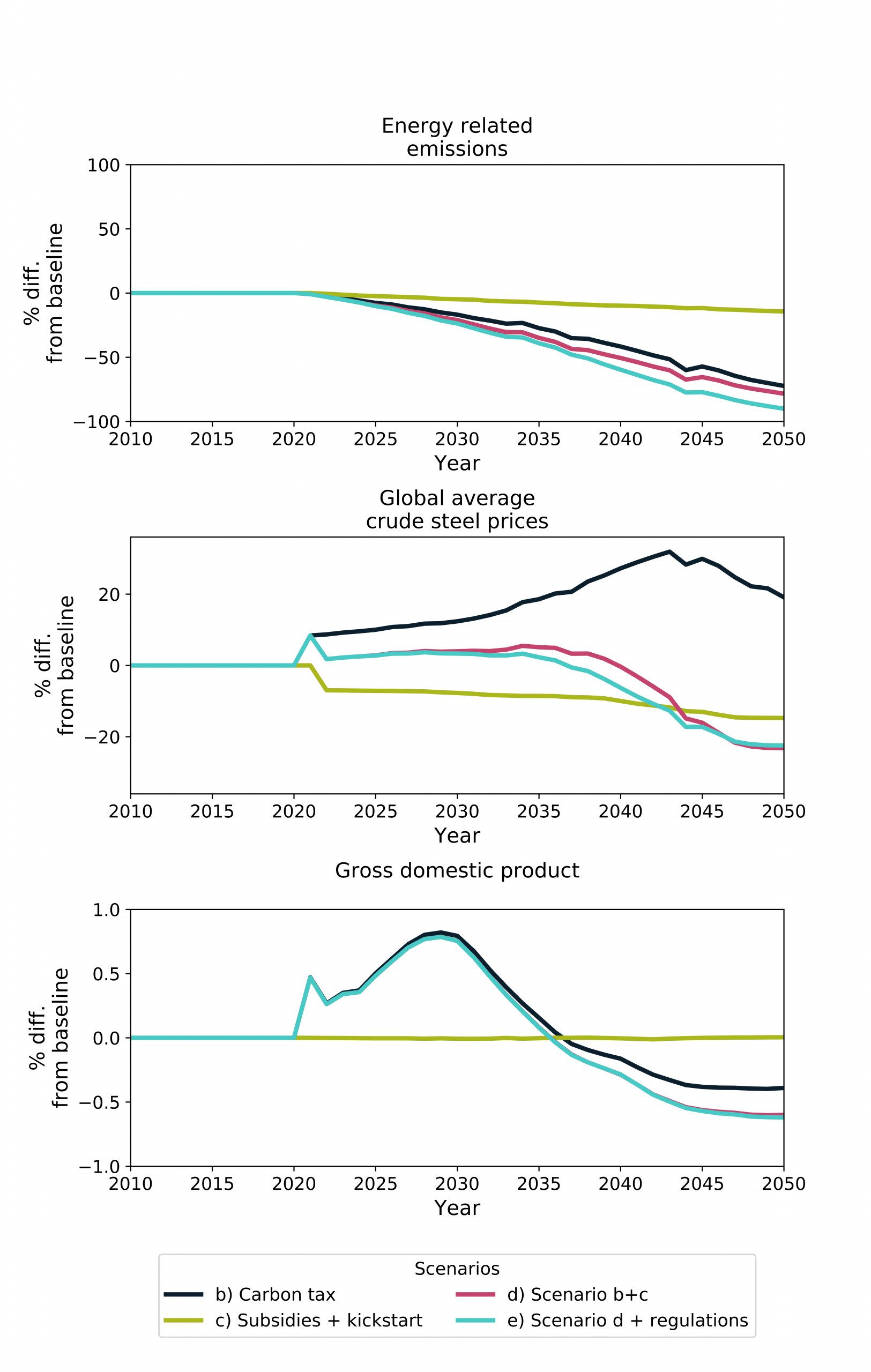

Of course, enacting these policies with the purpose of altering the course of technology uptake will have environmental and economic consequences, which are shown in figure 2. The carbon tax policies are most effective in lowering emissions, while the subsidies along with a kickstart policy do little in terms of emission reduction. However, when used in combination there seems to be a synergy. The addition of regulation will lower emissions even further as it creates more space for low-carbon technologies.

Figure 2: Differences in emissions, steel prices, and GDP compared to the baseline as a result of the enacted policies.

As carbon taxes rise, so too will the costs of steelmaking via carbon intensive technologies. Without subsidising low carbon production (scenario b), the price of steel increases up 32% compared to the baseline around 2043 and it comes down afterwards due to learning-by-doing effects but remains above baseline levels. The scenarios that also include low-carbon support (scenarios d and e) show an initial increase in steel prices due to the carbon tax, but hovers slightly above baseline levels up to 2040 due to subsidies being accounted for in determining the price. Afterwards, learning-by-doing effects push the prices below the baseline levels. These effects are more pronounced compared to the scenario with just supporting policies (scenario c): Carbon taxes and regulations push out the mature and carbon-intensive production in favour of subsidised production.

The GDP results in any scenario incorporating an economy-wide carbon tax go through two phases: 1) an initial investment boost, and 2) a debt repayment phase. The latter is characterised by higher prices of most commodities and services due to the carbon tax covering all sectors (not shown in the graphs) and reduces overall consumption. Our scenarios show that the investment boosts dominate first, then the consumption response to prices takes over and leads to minor but negative GDP outcomes towards 2050. A policy package that only focusses on low-carbon support (scenario c) will have negligible effects on GDP as it is strictly focussed on the iron and steel industry and does not affect others cogs in the economic machine directly.

So, is carbon-neutral steel-making possible?

As we have seen using Cambridge Econometrics’ latest addition, FTT:Steel, near carbon-neutral steel IS a possibility. Policies are very likely able to change technology uptake in the steel sector, thereby cutting down emissions at some costs.

Yet, decarbonisation is not as simple as imposing a carbon tax, which is a general conclusion we find at Cambridge Econometrics.

Complete decarbonisation of the steel sector would require a more stringent policy portfolio than portraited above. The addition of FTT:Steel allows us to increase our analytical power of policies related to the steel sector. Another example where applied FTT:Steel can be found here.

Disclaimer 1: This blog post was updated on the 18th of June 2021, due to cumulative model updates of E3ME and FTT:Steel and to improve the visualisation of the results. Overall, the narratives of the scenarios have remained the same.

Disclaimer 2: Our approach deviates from finding an ‘optimal’ outcome. Instead, it represents ‘real world’ policy choices faced by policy makers. Our simulation results provide insights to likely impacts of policy intervention.

Great post ! Liked the concept of making steel from use of carbon. This is innovative and cost effective solution. For steel and metal fabrication we must need the good quality steel supplies that will be leads to make best project work.